During South Korea’s growth miracle decades, firm concentration rose sharply. The largest firms powered the rise in concentration and contributed to the growth miracle.

Editor’s note: For a broader synthesis of themes covered in this article, check out our VoxDevLit on Industrial Development.

Large, dominant firms can be superstars or supervillains. As superstars, their expansion can reflect superior productivity and innovation, raising aggregate output and living standards. As supervillains, they can instead hamper growth and welfare, disproportionately raising prices, suppressing wages, and stifling business dynamism. Rising firm concentration in high-income economies has intensified this debate on both sides (Autor et al. 2020, De Loecker et al. 2020, Covarrubias et al. 2020, Kwon et al. 2024).

The empirical evidence on the role of large firms in low- and middle-income countries remains thin, while policy stances have varied sharply. Some governments – India under the License Raj is a prominent example – explicitly suppressed large firms. Other cultivated them. Indeed, several of the most spectacular growth episodes of the last century featured very large, internationally competitive national champions: Sony and Toyota in postwar Japan, Samsung and TSMC in Korea and Taiwan, and BYD and Huawei in China today (Amodio et al. 2026).

Whether concentration helped or hurt long-run growth in these settings is an empirical question that has been difficult to answer due to lack of long-horizon firm-level data.

South Korea’s growth miracle and rising concentration

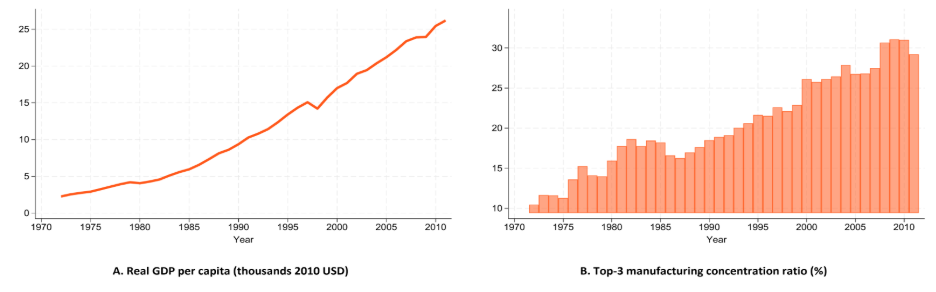

In recent work (Choi, Levchenko, Ruzic, and Shim 2026), we revisit one of the most spectacular growth episodes of the twentieth century – South Korea’s growth miracle between 1972 and 2011 – using historical firm-level data covering this time horizon for the first time. Over these four decades, Korea’s real GDP per capita rose nearly twelvefold, an average growth of 6.5% per year. A country whose top export in the late 1960s was human-hair wigs ended the period producing some of the world’s most advanced semiconductors, ships, and cars.

Figure 1: Real GDP per capita and Top-3 manufacturing concentration in South Korea, 1972–2011

The headline growth rate is well known, but the change in firm concentration along the way less so. We find that the sales share of the top three firms in each manufacturing sector rose from about 10% in 1972 to nearly 29% in 2011.

Productivity, not subsidies

Did Korea’s largest firms grow big because of government favouritism, or because they became more productive over time? To tell these stories apart, we build a quantitative model of heterogeneous firms with market power in both product and labour markets, idiosyncratic distortions, and selection into exporting. Each Korean firm we observe is an object in the model. We invert the model to recover four firm-level shocks: productivity, foreign demand, labour distortions, and capital distortions. We identify firm-level shocks by matching the model to each firm’s observed sales, employment, capital, and export shares.

We have two main findings. First, the top three firms experienced exceptional productivity growth. In 1972, they were on average about 2.3 times more productive than other firms in their sector. By 2011 the gap had widened to 8.8 times. Second, the distortions facing the top three firms, relative to others, do not exhibit obvious trends over the long run. Large firms in heavy manufacturing were relatively more subsidised for their capital usage during the Heavy and Chemical Industry Drive of 1973–1978 (Choi and Levchenko 2025, Kim et al. 2021), but most of that preferential treatment had dissipated by the 1990s. Subsidies are not what made the large firms big in the long run. Productivity did.

How much did the top large firms matter?

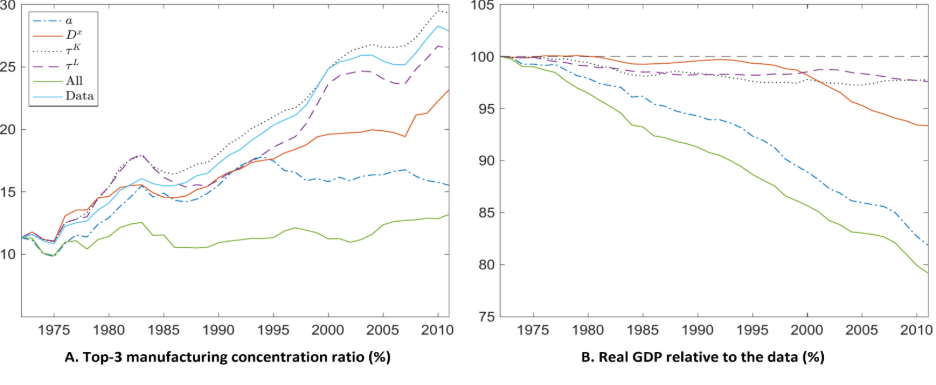

What would Korean GDP and welfare have looked like had the top three firms grown like a typical firm in their sector? To answer this, we run a counterfactual in which the top three firms’ productivity, foreign demand, and wedges grow at the average rate of similarly aged firms in the same industry.

Without the differential performance of the top three firms, Korean real GDP per capita in 2011 would have been 20.8% lower, and the net present value of welfare over the whole period 6.6% lower. Most of this is due to productivity. Shutting down the top three’s faster productivity growth alone leaves 2011 GDP 18.1% lower and welfare 4.9% lower.

A natural concern is that larger firms have higher markups and markdowns. But average markups and markdowns rose only slightly over four decades. Aggregate productivity, by contrast, rose by about 50%.

Figure 2: The impact of top-3 micro shocks

A single firm – Samsung Electronics – accounts for roughly a third of the total effect. Had Samsung’s shocks evolved at the average rate, Korean 2011 GDP would have been about 7% lower and welfare 1.2% lower. For Hyundai Motors, the same impacts would be 0.7% and 0.9%. Individual companies can thus have a measurable impact on an entire country’s long-run growth (Gabaix 2011, di Giovanni and Levchenko 2012).

Superstars vs. supervillains

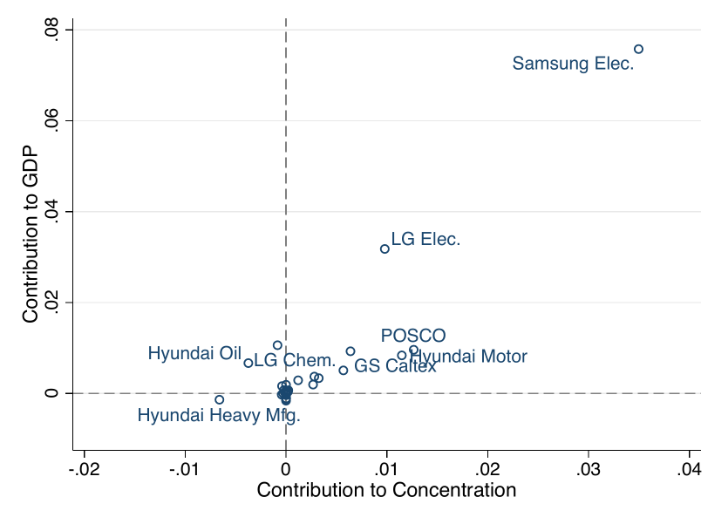

Figure 3: The impact of micro shocks for each top-3 firm

Figure 3 plots each top-3 firm’s contribution to concentration (horizontal axis) against its contribution to real GDP (vertical axis), with each dot representing one firm. Firms in the upper-right quadrant are superstars: they outperformed peers and contributed positively to growth. Samsung Electronics and Hyundai Motors are among them. Firms in the lower-right would be supervillains: they raise concentration but lower GDP. Almost no Korean top-3 firm sits in that quadrant.

Korea’s largest firms were overwhelmingly superstars, not supervillains. Superstars account for 21% of aggregate sales by 2010; supervillains account for just 0.1%. We also stress-test this conclusion. The result survives when we account for mergers and acquisitions (which could mechanically inflate top-firm sales), for productivity spillovers to other firms, and for a range of alternative parameter values. The pattern is robust: in Korea, the firms that grew biggest were also the ones that contributed most to the growth miracle.

Policy implications for industrial development

Three lessons stand out for the development policy debate.

- First, individual firms matter. Samsung Electronics alone explains roughly a third of the top-3 contribution to Korean GDP. Development accounting that works only with sectoral aggregates can miss that kind of granularity.

- Second, big can be good, but only under the right conditions. Concentration on its own is uninformative about welfare. Whether large firms are superstars or supervillains depends on why they got big, an empirical and quantitative question whose answers are surely country- and time-specific.

- Third, distortions or regulations that suppress growth of productive national champions can hurt long-run growth. In fact, World Bank (2024) recommends that low- and middle-income countries “move away from coddling small firms or vilify large firms”.

References

Amodio, F, M Poschke, B Caprettini, J Choi, H Huang, Y-H Lei, T Reed, R Rodrigo, L F Sáenz, M Sanfilippo, M Schwartzman, G de Souza, M Sposi, and V Wiedemann (2026), "Industrial development," VoxDevLit, 1(1).

Autor, D, D Dorn, L F Katz, C Patterson, and J Van Reenen (2020), "The fall of the labor share and the rise of superstar firms," Quarterly Journal of Economics, 135(2): 645–709.

Choi, J, and A A Levchenko (2025), "The long-term effects of industrial policy," Journal of Monetary Economics, 152: 103779.

Choi, J, A A Levchenko, D Ruzic, and Y Shim (2026), "Superstars or supervillains? Large firms in the South Korean growth miracle," NBER Working Paper No. 32648.

Covarrubias, M, G Gutiérrez, and T Philippon (2020), "From good to bad concentration? US industries over the past 30 years," NBER Macroeconomics Annual, 34: 1–46.

De Loecker, J, J Eeckhout, and G Unger (2020), "The rise of market power and the macroeconomic implications," Quarterly Journal of Economics, 135(2): 561–644.

di Giovanni, J, and A A Levchenko (2012), "Country size, international trade, and aggregate fluctuations in granular economies," Journal of Political Economy, 120(6): 1083–1132.

Gabaix, X (2011), "The granular origins of aggregate fluctuations," Econometrica, 79(3): 733–772.

Kim, M, M Lee, and Y Shin (2021), "The plant-level view of an industrial policy: The Korean heavy industry drive of 1973," NBER Working Paper No. 29252.

Kwon, S Y, Y Ma, and K Zimmermann (2024), "100 years of rising corporate concentration," American Economic Review, 114(7): 2111–2140.

World Bank (2024), World Development Report 2024: The Middle-Income Trap, World Bank, Washington, DC.