A large temporary cash incentive rapidly enrolled millions of informal workers into Thailand's voluntary social insurance programme, demonstrating that enrolment barriers can be overcome when incentives are strong enough. However, the high dropout rate and choices made at sign-up suggest that low baseline enrolment reflects a genuine lack of demand for the product, with important implications for how governments design and promote social insurance schemes.

Worldwide, many countries provide social insurance to help citizens manage retirement, disability, or death of a family member. In high income countries, social insurance enrolment and payments are linked to payroll taxes at work, covering large segments of the population. However, this type of strategy runs into real challenges in many low- and middle-income countries, where a large fraction of workers are engaged in informal sector employment. As a result, while many developing countries still cover formal workers through payroll taxes, for informal workers, many governments have instead created opt-in, contributory systems, in which workers must pay their premium directly to the government each month. This opt-in system, however, has led to typically low enrolment and high dropout rates (Banerjee et al. 2024).

Why do few people enrol? Perhaps the simplest explanation is that people just do not know about the insurance. But suppose that they do know about it and want to enrol – it could also be that they cannot afford it. Or they can afford it, but the hassles of putting together the paperwork, standing in lines to enrol, or interacting with government bureaucrats during the process may deter them (Banerjee et al. 2021). They may also know about the insurance, but just not want it because the insurance product is a bad deal in an actuarial sense or, even if it is a good deal financially, they may simply not value it (Finkelstein et al. 2019).

Understanding why enrolment is low is essential when designing social insurance programmes. Therefore, we studied these questions in a unique policy experiment in Thailand, in which the government offered large incentives for informal workers to voluntarily enrol in the national social insurance programme for non-formal workers, referred to as Social Security Article 40.

Article 40 has three options, ranging in cost and generosity of benefits. Option 1 costs THB 70 per month (US$1.9) and offers a basic package of compensation for loss of work income due to illnesses, disability benefits, and death benefits; Option 2 costs THB 100 ($2.7) per month and adds a pension benefit; and Option 3 costs THB 300 ($8) per month and adds a child allowance benefit for up to two children, while also providing higher coverage for the loss of work, disability, and death benefits. The insurance itself is affordable: the cheapest option is about 1% of earnings, even for households in the lowest income quintile. By comparison, 50–60% of Thai households participate in lottery or gambling, spending around THB 120–300 per month. This suggests that affordability or liquidity constraints are not the key barrier to participation.

Studying voluntary social insurance enrolment in Thailand

The unusual policy experiment we study occurred in July–August 2021, when, as part of the COVID-19 response, the government offered large lumpsum grants to informal workers in 29 out of 77 provinces. The government distributed the grants through the Thai Social Security System, and so to receive a grant, people needed to be enrolled in Article 40. Crucially, those who were not currently enrolled in Article 40 were given an opportunity to do so before the payments were disbursed.

These grants therefore provided a large incentive to enrol in Article 40. Informal workers who lived in these 29 provinces were eligible to receive either THB 5,000 for one month ($134) or THB 5,000 for each of two months ($268 total), depending on the province. To put this in perspective, the Thai minimum wage is about THB 7,500 per person per month. Those in other provinces were ineligible.

To understand the impact of the incentive, we use de-identified, individual-level administrative data from the Thai Social Security Office (SSO) from May 2011 to April 2024 (Olken, Hanna, Poonpolkul, and Wasi 2026). The data covers both eligible and ineligible provinces, allowing us to compare the two groups over time. We complement this data with information from the Thai Labor Force Survey to assess the overall coverage of the scheme.

What was the impact of the incentives on enrolment?

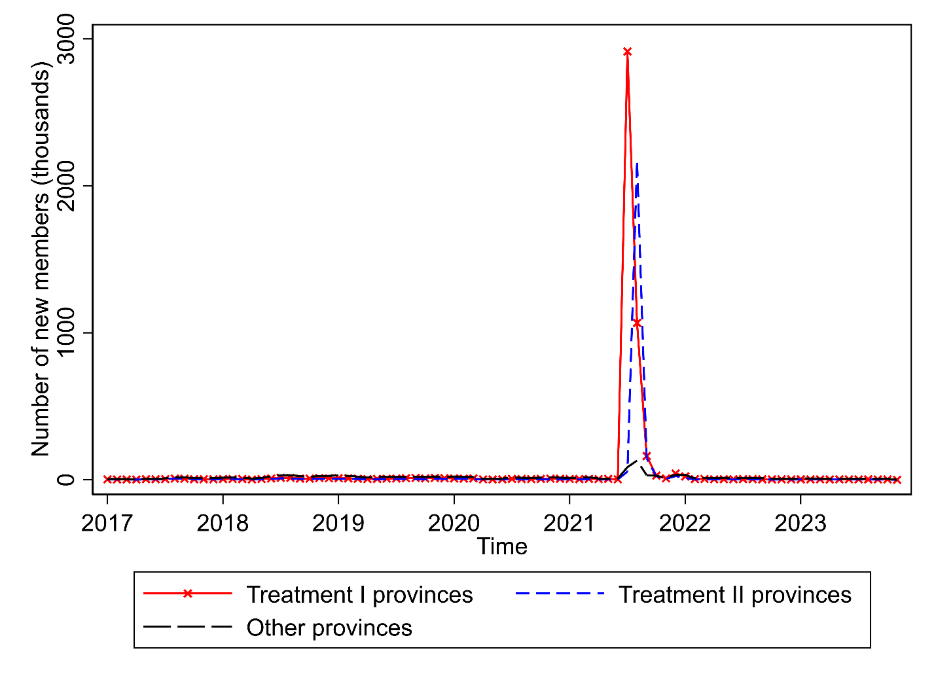

Given such a strong cash incentive, if administrative capacity was not a constraint, and information was widespread, we would expect large numbers of people in eligible provinces to enrol – we saw exactly that. As shown in Figure 1, in just two months, over six million people enrolled. To put this in perspective, during the four years prior to this, from 2017 to 2021, only about 30,000 people enrolled in a typical month from these provinces.

Figure 1: Article 40 enrolment

This large enrolment spike meant that a large fraction of informal Thai workers was covered in these provinces, as the share increased from about 6% to 73% in just two months. This is our first key result: the fact that millions enrolled quickly suggests that administrative and other enrolment barriers did not prevent enrolment, especially if the incentives to do so were large enough.

Do people value the insurance enough to remain enrolled after the incentives end?

If low enrolment is mostly due to a one-time fixed enrolment cost, but people value the insurance on an ongoing basis, then once the incentive brings people into the system, they should remain enrolled in the programme. However, if they do not value the insurance, they may drop the insurance as soon as they receive the lump-sum grant.

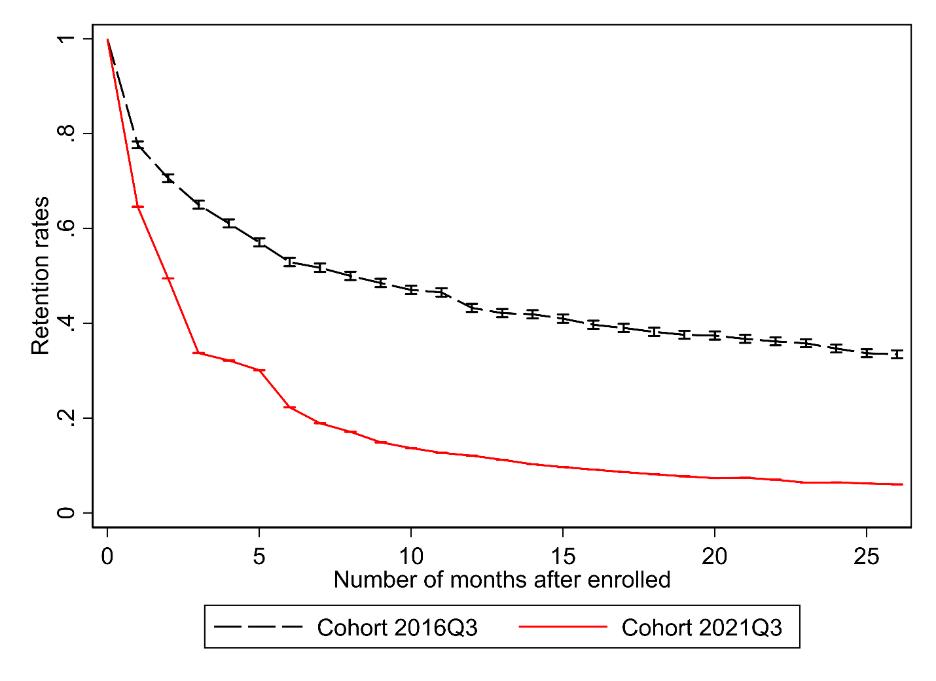

We find the latter: many people let their insurance lapse (see Figure 2) – and those who dropped coverage did so at a much higher rate than people who joined prior to the large incentives. Within six months, only 24% remained enrolled, much lower than the comparable retention rate for those who joined prior to the incentives (53%). A year later, only 13% of those who enrolled due to the incentives kept their insurance coverage, compared to 43% who enrolled during the non-incentive period. Even so, despite these decreases, in aggregate, the incentives substantially increased total enrolment – simply because so many millions of people enrolled.

Figure 2: Retention rates of those joining Article 40 in the third quarter of 2016 and 2021

What drives social insurance enrolment?

The lower retention rate could reflect a low net valuation of the insurance in two ways. First, those induced to enrol due to the incentives could discover, over time, that the insurance was less valuable to them, or that paying monthly was more challenging than they expected. Or, they could have known from the start: that is, they knew they had a low valuation of the insurance, and hence never enrolled before the incentives were introduced. To investigate whether this reflects ex-ante knowledge, we exploit the fact that Article 40 comes in three different tiers, with higher tiers having both higher premia and benefits. For example, the top two tiers include retirement benefits, with the highest tier including a child allowance. Premia for each tier are the same for everyone, but the expected tier benefits differ based on age and gender.

We model the benefits from each tier as a function of an individual's age and gender (similar to Landais et al. 2021). We then use this model to see whether those who are induced to enrol due to the incentive make systematically different choices than those who enrol without it. We find that they do: those who enrol without the subsidy make choices consistent with them valuing the insurance benefits much more than those who enrol during the incentive period. That is, the people induced to join by the large temporary incentives seem to know, ex-ante, that they value the insurance less, and choose accordingly. In fact, we find that without the subsidy, most people enrol in option two, which provides many with the highest value of benefits relative to cost. In contrast, with the subsidy, many just choose option one, the cheapest option to get the incentive.

Policy implications for social insurance

In short, given a substantial financial incentive, one can enrol most informal workers into social insurance almost immediately: in this case, millions of people enrolled within weeks. However, those that signed up did so knowing they were unlikely to want to maintain the insurance post the incentive; they chose the least expensive insurance tier with the fewest benefits, and then they dropped out at very high rates. The barriers to enrolment, therefore, seem to reflect in part a cost-benefit calculus on the part of potential beneficiaries, rather than necessarily reflecting high enrolment costs or administrative barriers.

References

Banerjee, A, A Finkelstein, R Hanna, B A Olken, A Ornaghi, and S Sumarto (2021), "The challenges of universal health insurance in developing countries: Experimental evidence from Indonesia’s National Health Insurance," American Economic Review, 111(9): 3035–3063.

Banerjee, A, R Hanna, B A Olken, and D Sverdlin-Lisker (2024), "Social protection in the developing world," Unpublished manuscript.

Finkelstein, A, N Hendren, and M Shepard (2019), "Subsidizing health insurance for low income adults: Evidence from Massachusetts," American Economic Review, 109(4): 1530–1567.

Landais, C, and J Spinnewijn (2021), "The value of unemployment insurance," Review of Economic Studies, 88(6): 3041–3085.

Olken, B A, R Hanna, P Poonpolkul, and N Wasi (2026), "Willingness-to-pay versus administrative hurdles: Understanding barriers to social insurance enrollment in Thailand," Review of Economics and Statistics, 1–27.