Global evidence from 33,262 mining sites shows that mineral price booms increase deforestation in nearby areas, beyond immediate mine sites. Investor origin shapes the size of these effects: mines owned by investors from higher-income countries generate lower deforestation responses, especially in lower-income host countries.

Editor’s note: For a broader synthesis of themes covered in this article, check out our VoxDevLit on Deforestation.

Deforestation contributes to around 20% of greenhouse gas emissions every year and is a major contributor to climate change (Van der Werf et al. 2009). Preserving forest cover is widely seen as one of the most cost-effective ways to mitigate climate change, while also protecting biodiversity and potentially improving human health. Yet deforestation rates remain high, in part because governments and communities often face trade-offs between economic development and sustainability.

These trade-offs are becoming increasingly important as the global demand for minerals rises. The clean energy transition, the growing need for energy storage, and the critical role of minerals in global supply chains have intensified the search for mineral resources around the world. This is not the first such wave: the early 2000s commodity super-cycle, driven by rapid growth in emerging economies such as China and India, generated sharp exogenous shocks in mineral prices. Mining contributes to deforestation directly, as trees are cleared for extraction, and indirectly, as mining activity induces nearby urban expansion, land use changes, and other local economic activity. The deforestation effects of mining may also depend on where investors come from.

As the global search for critical minerals continues (Hendrix 2023), and as cross-border investment increasingly comes from developing countries, understanding the environmental impact of mining on local communities and how mine investor origin characteristics affect the magnitude of such impact is crucial. Yet these questions have not been thoroughly addressed in the existing literature, because of challenges in causal identification and data availability.

Using the commodity boom to study mining and deforestation

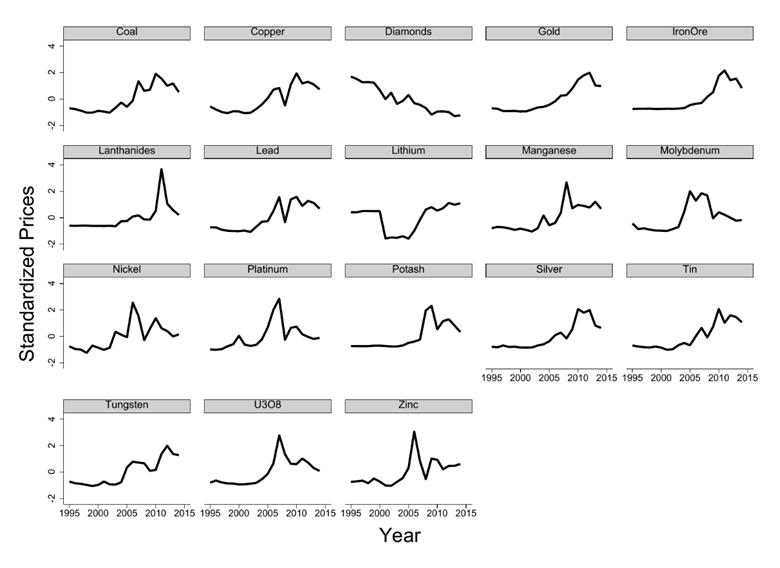

The early 2000s global commodity boom provides an opportunity for us to study how mining expansion affects deforestation worldwide (Xie, You, and Goldblatt 2025). To do so, we assemble a new global dataset covering 33,262 mining sites across 159 host countries, with information about the mines’ investors from 139 countries, linked to high-resolution satellite imagery measuring forest cover change (Hansen et al. 2013). Figure 1 illustrates the extensive geographic coverage of the analysis sample, spanning major mining regions around the world. Figure 2 shows the commodity price shocks during the global commodity super-cycle starting in 2000, which provide the empirical variation we exploit for identification.

Figure 1: Global mining sites

Figure 2: Standardised prices of major commodities

Do mineral price shocks lead to forest loss?

Our empirical strategy combines mine-level information on minerals extracted with cross-mineral variation in global commodity prices. Because individual mines are price takers in global markets, these demand-driven price shocks provide plausible variation in mining activity. We find that mining expansion significantly increases deforestation around mining sites: a one-standard-deviation increase in mineral prices raises forest cover loss by about 0.5 percentage points within 1 km of mines and 0.14 percentage points within 30 km. Our estimates suggest that the commodity super-cycle contributed to approximately 5.7% of total deforestation within 30 km of mining sites worldwide between 2000–2014.

The role of mining investor origin

Although much of the previous evidence has focused on the role of host-country characteristics in shaping cross-border environmental impacts, we find that these characteristics explain relatively little in our study context. Among cross-border-owned mines, we test whether the elasticity of forest cover loss varies with host-country rule of law, corruption, environmental performance, and demand proximity. Most of these host-country characteristics have limited effects on the deforestation behaviour of cross-border mining investors. Host country GDP per capita is the only factor that modestly affects the elasticity of deforestation to mineral prices.

By contrast, investor origin matters substantially. Mines owned by investors from higher-income countries exhibit significantly lower deforestation responses to mineral price shocks, and this pattern remains even after controlling for host-country income. In the 30 km buffer zone, a one-log-point increase in the GDP per capita of the mine owner’s country is associated with a 0.168 decrease in the price elasticity of forest cover loss. The role of investor origin is especially important in lower-income host countries.

How investor origin shapes local economic spillovers

Why are mines owned by investors from higher-income countries associated with less deforestation? To disentangle the mechanisms, we bring in additional microdata from nighttime lights and IPUMS, as well as other country-level indicators. The evidence suggests that this pattern is partly driven by differences in local economic spillovers: when mineral prices rise, areas surrounding these mines experience relatively smaller declines in manufacturing employment and higher levels of local economic activity, as measured by nighttime lights. These activities are typically less land-intensive than alternatives such as agricultural expansion, reducing the need for forest clearing. We also find suggestive evidence that institutional quality and environmental norms may be transmitted from investors’ home countries. By contrast, these differences do not appear to arise because investors from higher-income countries systematically select different mines or locations, use more advanced technologies, have better access to finance, or face stronger external scrutiny from regulators and the public. Overall, our results show that investor origin can matter even more than where mining investment takes place in shaping the environmental consequences of resource extraction.

Policy implications for deforestation

Despite the importance of forest preservation, deforestation rates remain high and are sensitive to both economic conditions and institutional factors (Balboni et al. 2023). Our results show that mining price shocks induce significant deforestation, with impacts extending beyond mine sites to surrounding regions. We also show that ownership matters: the environmental impact of mineral price shocks depend not only on where a mine is located, but also on who owns it. This is especially important for cross-border mining investment in lower-income countries, where investor origin plays an even more pronounced role in shaping deforestation outcomes.

As demand for critical minerals grows, policymakers can benefit from looking beyond mining methods and environmental practices within mine sites. In mineral-rich countries, policy design should also pay attention to the types of local economic activity generated by mining booms and busts, the associated land-use changes, and the environmental externalities for nearby communities. This perspective can help countries benefit from rising mineral demand while curbing local environmental costs.

References

Balboni, C, A Berman, R Burgess, and B A Olken (2023), "The economics of tropical deforestation," Annual Review of Economics, 15: 723–754.

Hansen, M C, P V Potapov, R Moore, M Hancher, S A Turubanova, A Tyukavina, D Thau, et al. (2013), "High-resolution global maps of 21st-century forest cover change," Science, 342(6160): 850–853.

Hendrix, C (2023), "Made in America puts the brakes on electric vehicles Biden hopes to push," Peterson Institute for International Economics.

Van der Werf, G R, D C Morton, R S DeFries, J G J Olivier, P S Kasibhatla, R B Jackson, G J Collatz, and J T Randerson (2009), "CO2 emissions from forest loss," Nature Geoscience, 2(11): 737–738.

Xie, V W, W You, and R Goldblatt (2025), "Investor origin and deforestation: Evidence from global mining sites," Review of Economics and Statistics, 1–28.