Audits do more than recover unpaid taxes. New evidence from South Africa suggests that they also increase tax reporting by audited firms’ geographic neighbours and by other clients of the same tax practitioner. This implies that revenue collection could be strengthened if authorities moved beyond narrow audit strategies focused solely on immediate revenue gains and adopted broader enforcement designs that account for network compliance spillovers.

Tax evasion is a widespread phenomenon, especially in low-income countries (Besley and Persson 2014). It deprives governments of tax revenues required to finance much-needed public goods and services and can exacerbate inequality when those with greater opportunities to evade contribute less.

Do audits impact taxpayers‘ compliance behaviour?

Taxpayer audits are widely perceived to be a key instrument to combat tax evasion. They help recover unpaid taxes, but to what extent they deter taxpayer non-compliance is empirically unclear. Recent empirical research suggests that audits shape the post-audit tax compliance of audited taxpayers. Less research has examined, however, whether they also influence the tax reporting of the broader population of unaudited taxpayers.

This is not a small gap in the evidence base. The vast majority of taxpayers are never audited, so most of the deterrent value of audit programmes – if there is any – has to come from how audits change the behaviour of those they do not directly touch. While governments often withhold details on audit risk and selection rules from the broader public for strategic reasons (Bergolo et al. 2018), unaudited taxpayers may learn from audit experiences within their networks and adjust their compliance behaviour accordingly.

Understanding such audit responses – and their subsequent revenue consequences – is essential for governments to design effective tax audit schemes. Suboptimal use of administrative audit resources is thereby particularly costly in low-income countries, where the opportunity cost of assigning skilled staff to audit work is high and the benefits of additional tax revenue collection can be large.

Yet evidence on audit spillovers into taxpayer networks is thin and confined to high-income economies. Boning et al. (2020) and Battaglini et al. (2025) find that audits propagate through the networks of professional tax advisors. Whether such patterns travel to lower-income-country settings with weaker public institutions and less professional tax-preparer markets remains an open question.

Identifying network compliance spillovers

In recent research (Lediga, Riedel, and Strohmaier 2026), we use rich tax administrative data from South Africa to assess if tax audits affect the behaviour of unaudited fellow taxpayers in the same network, focusing on corporate income tax. We link the universe of corporate tax returns to the universe of corporate tax audits conducted by the South African Revenue Service. This allows us to test for potential audit spillovers in two network dimensions: local neighbourhoods and tax practitioner networks.

Methodologically, we use on a difference-in-differences design, comparing changes in tax liability reporting among firms exposed and unexposed to audits in their local or tax practitioner networks at a given point in time. The main identification challenge is that audits are not randomly allocated across taxpayers but conditioned on taxpayers’ expected non-compliance risk, which may – if tax reporting trends are correlated within networks – act as a confounder in the analysis. We address this through multiple approaches – including leveraging our exceptionally rich administrative tax data to compare treated with untreated taxpayers, who are observationally identical across a granular set of characteristics.

Audits ripple through local and tax practitioner networks

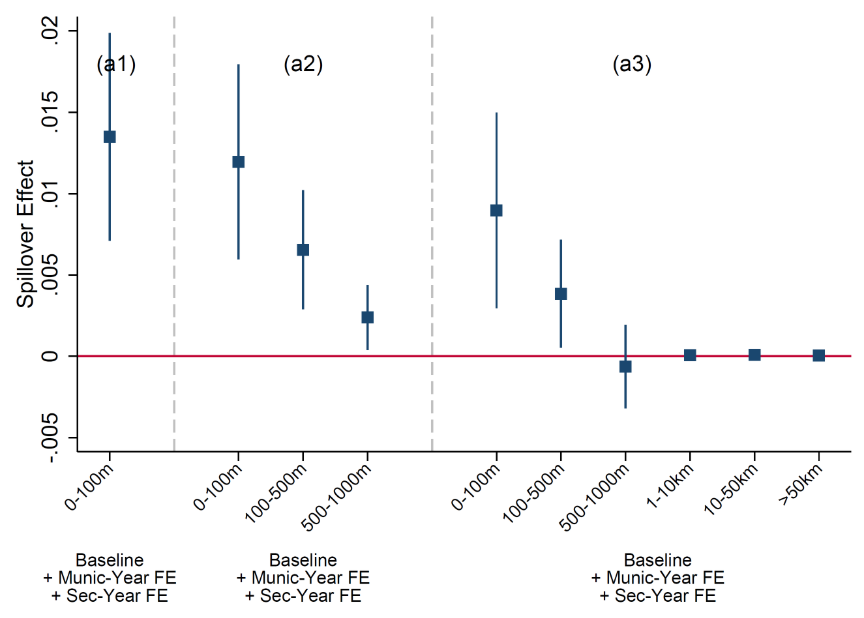

Our findings point to sizeable positive spillover effects in both network domains. The tax liability reporting of untreated businesses, on average, increases by around 1% when a neighbouring firm within a 100-metre radius is audited. The spillovers extend to larger distance bands and several post-audit periods but intuitively decline in space and time (Figure 1). Similar effects emerge in tax practitioner networks: being exposed to an additional network audit increases the tax reporting of non-audited firms by around 1% – with the effect persisting over time. Because taxpayers are connected to multiple others across both networks, these compliance responses translate into aggregate revenue gains comparable in size to the direct recovery of unpaid taxes during the audits.

Figure 1: Audit enforcement spillovers in local taxpayer networks

Notes: The figure depicts the effect of experiencing a neighbour audit in the indicated distance radius on taxpayers’ inverse-hyperbolic-sine transformed tax liability. Panel (a) accounts for the effect of neighbouring audits in a distance of 0-100m only, Panel (b) for the effect of neighbouring audits in a distance-radius of 0-100, 100-500m, 500-1000m and Panel (c) for the effect of neighbouring audits in a distance-radius of 0-100, 100-500m, 500-1000m, 1-10km, 10-50km and >50km respectively.

We further document relevant heterogeneity in reporting adjustments, finding that responses are especially pronounced when taxpayers are rarely exposed to taxpayer audits in their networks. This is consistent with the notion that, in such cases, the information value of an additional audit is high, making audits especially likely to trigger deterrence responses.

Underlying transmission channels differ by network type

The structure of network spillovers differs sharply between local and tax practitioner networks. In the former, the spillover effects are driven by tax audits that resulted in an upward adjustment of audited taxpayers’ assessed tax liability, that is, audits in which taxpayers were found to be compliant. In tax practitioner nets, the opposite holds true: audit spillovers are driven by tax audits in which taxpayers were identified as non-compliant, that is, audits that did result in upward adjustments of the assessed tax liability.

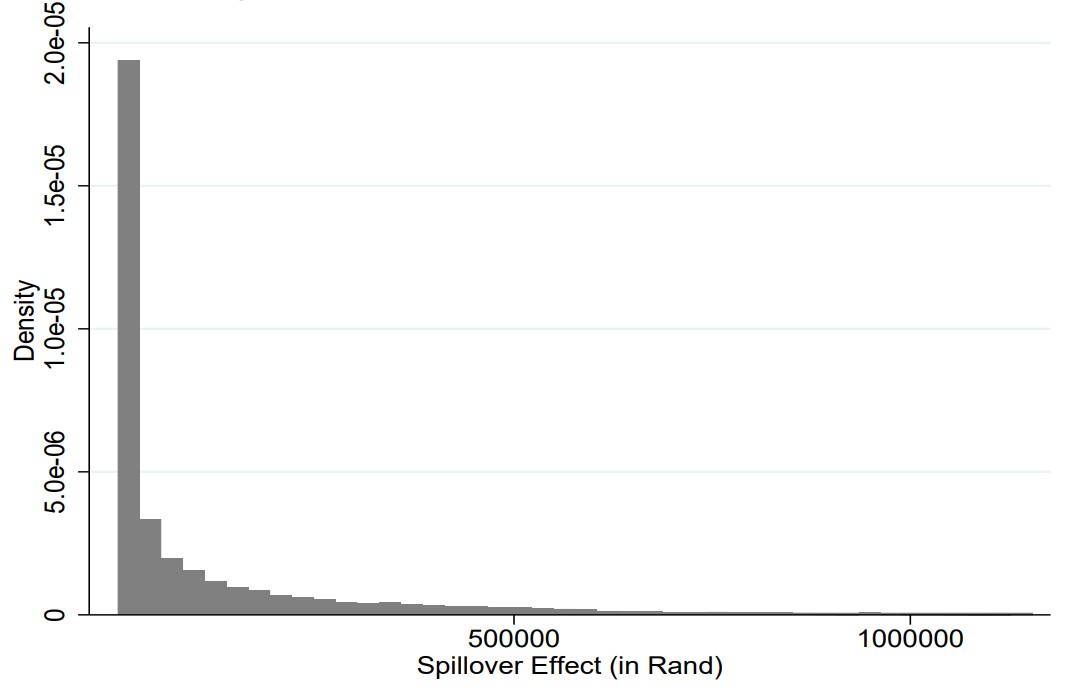

Figure 2: Network spillovers per audit

Notes: The figure depicts the distribution of the network spillover effects (accounting for both spillovers in local and in tax practitioner networks) for all corporate taxpayer audits during our data frame.

These patterns are consistent with neighbourhood spillovers that are governed by strategic communication. A firm identified as non-compliant has little incentive to disclose the audit. A firm cleared by the auditor is more likely to share the experience, credibly signalling that it complies with tax obligations. This predicts that network spillovers will be concentrated among audits in which taxpayers are cleared – consistent with our empirical evidence.

Tax practitioners, in turn, learn about audit outcomes regardless of the result, and face reputational and licensing risks if their clients are repeatedly caught evading. In grey areas of tax law, they have incentives to revise tax schemes for all of their clients once they learn that they fail to be accepted by the tax authority. Tax practitioners may thus sharply adjust their counselling practice when one of their clients is caught evading – consistent with our empirical evidence.

A case for redesigning tax audit systems

Our findings have important implications for the design of tax enforcement schemes in low-income economies. Most tax authorities currently select audit cases to maximise immediate audit returns (Bloomquist 2013). Our findings suggest that this captures only part of the value at stake. Audits also improve the tax compliance of unaudited fellow taxpayers in local and tax practitioner networks, translating into sizeable additional revenue gains. This makes investments into audit capacity more attractive at the margin.

The size of an audit's network ripple also turns out to be largely uncorrelated with firm-level evasion signals used by standard audit case selection systems. Audits that appear most attractive on a narrow cost–benefit basis may thus not be those with the largest broader revenue effects. Incorporating taxpayers‘ network exposure into audit selection can therefore increase deterrence and help governments raise additional revenue.

References

Battaglini, M, L Guiso, C Lacava, and E Patacchini (2025), "Tax professionals and tax evasion," Journal of the European Economic Association, forthcoming.

Bergolo, M, R Ceni, G Cruces, M Giaccobasso, and R Perez-Truglia (2018), "Misperceptions about tax audits," American Economic Association Papers and Proceedings, 108: 83–87.

Besley, T, and T Persson (2014), "Why do developing countries tax so little?" Journal of Economic Perspectives, 28(4): 99–120.

Bloomquist, K M (2013), "Incorporating indirect effects in audit case selection: An agent-based approach," IRS Research Bulletin: 103–107.

Boning, W C, J Guyton, R H Hodge, J Slemrod, and U Troiano (2020), "Heard it through the grapevine: Direct and network effects of a tax enforcement field experiment," Journal of Public Economics, 190: 104261.

Lediga, C, N Riedel, and K Strohmaier (2026), "Tax enforcement spillovers: Evidence from business tax audits in South Africa," Economic Journal, forthcoming.